Managing personal finances is a vital part of everyday life. Years ago, financial planning was restricted to seeking advice from a bank manager or manually writing down calculations in a diary. Today, the modern Indian investor has access to online tools that make tracking money highly accessible.

At the center of this shift are online financial calculators. These automated tools allow you to project your future savings, calculate loan repayments, and view tax liabilities with mathematical accuracy. Whether you are just earning your first salary or optimizing an existing portfolio, utilizing a financial calculator helps you map out your financial trajectory. In this guide, we will explore the different financial calculators available in India, starting with the widely used SIP calculator, and understand how they assist in managing your money.

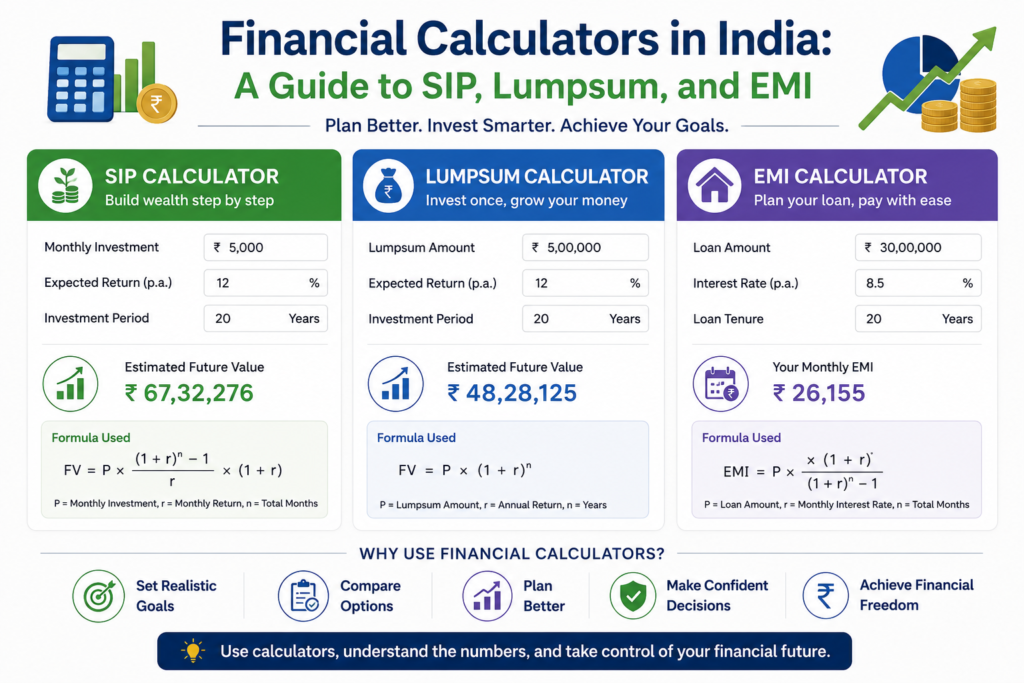

The Core Tool: The SIP Calculator

When it comes to building a portfolio in India, the Systematic Investment Plan (SIP) is a preferred method for many retail buyers. An SIP allows you to invest a fixed sum of money at regular intervals—usually once a month—into a chosen mutual fund. However, before you commit your capital, it is helpful to understand what those monthly allocations could look like over five, ten, or twenty years. This is where the SIP calculator serves as a practical asset.

An SIP calculator is a straightforward digital tool that projects the future value of your recurring monthly investments based on a specific, assumed rate of return. It removes guesswork from the equation. To use this tool, you need to input three basic figures:

- Your Monthly Investment Amount

- The Expected Annual Return Percentage

- The Total Investment Duration (in Years)

Within a moment, the calculator displays your total invested capital alongside the estimated wealth gained over time.

The primary benefit of the SIP calculator is that it demonstrates the long-term impact of compound interest. For instance, if you invest ₹5,000 every month for 20 years at an expected return of 12%, your total pocket contribution of ₹12,00,000 grows into an estimated final value of over ₹49,00,000. The calculator breaks down how a large portion of the final amount comes from the accumulated returns rather than your core principal. By adjusting the variables in an SIP calculator, you can establish clear milestones for specific goals, such as down payments, higher education, or an emergency fund.

Lumpsum Calculator: Deploying One-Time Capital

While an SIP is structured for regular monthly income, you may occasionally find yourself with a larger, single sum of money. This could happen when you receive a year-end performance bonus, an inheritance, or the proceeds from selling an asset like a car or property. In these instances, investing the money all at once is a standard strategy, and a lumpsum calculator is the appropriate tool to analyze it.

A lumpsum calculator operates on a similar mathematical foundation as an SIP calculator, but it focuses entirely on a single, one-time investment. By entering your initial principal, the expected rate of return, and your time horizon, the tool demonstrates how that single sum multiplies over the years. Because a lumpsum investment places your entire capital into the market from day one, the returns begin accumulating on the full amount immediately. Comparing the output of an SIP calculator against a lumpsum calculator helps you decide the most effective way to deploy your surplus cash based on your current liquid savings.

Traditional Savings: FD and RD Calculators

Despite the growth of market-linked investments, traditional fixed-income instruments like Fixed Deposits (FDs) and Recurring Deposits (RDs) remain popular cornerstones of Indian savings habits. They offer predictable returns and carry no market volatility, making them highly suitable for capital preservation and short-term targets.

An FD calculator determines the exact maturity amount and total interest you will earn on a one-time bank deposit. It processes the tenure, the specific interest rate offered by the bank, and the compounding frequency (whether monthly, quarterly, or annually).

Similarly, an SWP calculator operates like an SIP calculator but applies to risk-free bank deposits. It shows you how fixed monthly deposits accumulate interest over a set period. These calculators are widely utilized by conservative savers and senior citizens who rely on regular interest payouts to cover routine expenses without facing the ups and downs of the stock market.

Retirement Calculators: Preparing for the Long Term

Retirement planning is one of the longest financial commitments an individual will make. With rising living costs and healthcare expenses, building a dependable corpus requires early preparation. To manage this multi-decade timeline, several specific calculators are regularly used in India.

- The EPF Calculator: Essential for salaried corporate employees. It projects how your monthly Employees’ Provident Fund contributions, alongside the matching share from your employer, accumulate until retirement based on the annual interest rate set by the government.

- The PPF Calculator: For individuals seeking long-term tax benefits, the Public Provident Fund calculator is a standard choice. By inputting your yearly contributions, it tracks your capital growth over the mandatory 15-year lock-in period.

- The NPS Calculator: The National Pension System calculator estimates your final accumulated corpus at age 60 and outlines the potential monthly pension payouts based on your chosen annuity percentage.

Advanced retirement calculators also factor in average inflation, which helps you understand the actual purchasing power of your target retirement fund in today’s terms.

Debt Management: Loan and EMI Calculators

Financial planning is not just about growing your assets; it is equally about managing your liabilities. Whether you are taking out a home loan, financing a vehicle, or managing a personal loan for an emergency, knowing your exact repayment schedule is critical.

An EMI (Equated Monthly Installment) calculator is a basic utility that tells you exactly how much you must pay your lender every month. By inputting the total loan principal, the bank’s interest rate, and the tenure in years, the calculator instantly determines your monthly bill.

Furthermore, a comprehensive EMI calculator provides a detailed amortization schedule. This breakdown reveals how much of your monthly payment goes toward satisfying the bank’s interest charges versus how much actually reduces your core loan balance. Checking your numbers with an EMI calculator before signing a loan agreement allows you to adjust the tenure so your monthly payments fit comfortably within your ongoing household budget.

Tax Calculators: Evaluating Your Take-Home Income

Finally, navigating the tax structure is an essential part of personal finance in India. With choices between the Old and New Tax Regimes, calculating your actual liabilities requires careful comparison.

Income Tax calculators and Salary calculators allow you to estimate your exact tax burden based on your gross earnings, standard deductions, and specific exemptions like House Rent Allowance (HRA). Using a tax calculator early in the financial year allows you to determine how much you need to allocate to tax-saving avenues to optimize your net take-home pay legally.

Conclusion

Digital financial tools give modern retail savers total clarity over their money. Whether you are mapping out long-term returns with an SIP calculator, evaluating loan structures with an EMI calculator, or tracking tax-free growth with a PPF calculator, these free tools provide reliable answers. Developing a habit of checking your numbers regularly ensures your current budget aligns with your long-term milestones.

Frequently Asked Questions (FAQs)

Are online financial calculators accurate? Yes, online calculators use exact mathematical formulas to compute interest rates and payment schedules. However, for market-linked options like an SIP calculator, the output is a projection based on the “expected” return rate you enter. Because market returns vary daily, your actual final amount will look slightly different from the initial estimate.

What is the main difference between an SIP calculator and a Lumpsum calculator? An SIP calculator assumes you add a fresh, fixed amount of money to your investment every single month throughout the tenure. A lumpsum calculator assumes you invest a single chunk of money on day one and let it grow without adding any further funds.

Can I use a standard EMI calculator for a home loan and a car loan? Yes, the mathematical formula for computing an Equated Monthly Installment is universally the same. You can use the same calculator for home loans, car loans, or personal loans. You simply need to swap out the numbers for the specific interest rate and tenure required by your bank.